Sinking Funds Categories: The Smart Way to Plan for Future Expenses

Managing money becomes much easier when you stop treating every large expense like a surprise. That is where sinking funds can make a big difference. If you have ever felt stressed when a car repair, holiday shopping, annual insurance bill, or school expense suddenly appears, the problem is usually not that the expense was unexpected. The real issue is that the money was not set aside in advance. Learning about the right sinking funds categories can help you build a budget that is more realistic, stable, and less stressful.

A sinking fund is money you save little by little for a future expense. Instead of waiting until the bill arrives and then scrambling to cover it, you prepare for it ahead of time. This method helps you avoid debt, protect your monthly budget, and feel more in control of your finances. The key is choosing the sinking funds categories that match your life and spending habits.

What Are Sinking Funds?

Sinking funds are savings buckets for specific purposes. Each category is designed for an expense you know will happen at some point. These expenses may come monthly, yearly, seasonally, or only once in a while, but they are still part of your real financial life.

For example, if you know the holidays come every year, you can save a small amount each month in a Christmas sinking fund. If your car needs maintenance every few months, you can create a car repair fund. This keeps those costs from destroying your regular monthly budget.

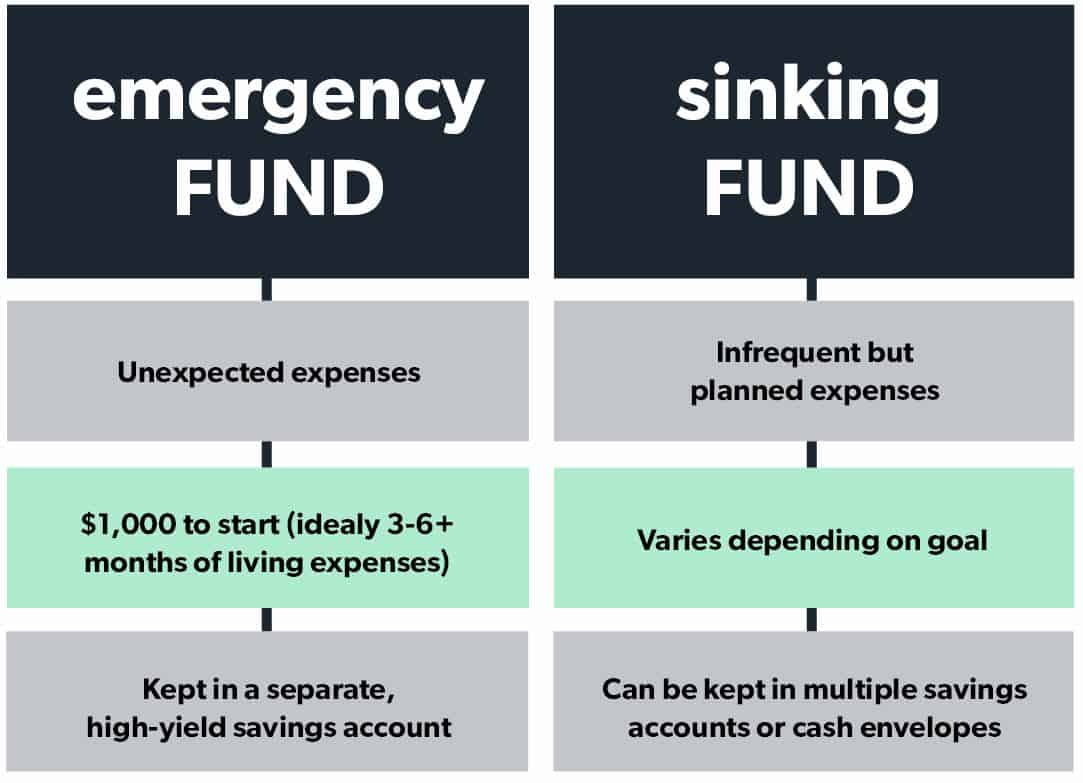

Unlike an emergency fund, which is meant for true unexpected situations, sinking funds are for planned or semi-planned expenses. They give every future dollar a job.

Why Sinking Funds Matter

One of the biggest reasons people struggle with budgeting is that they only plan for regular monthly bills. Rent, groceries, phone bills, and utilities get attention, but irregular expenses are often ignored. Then when those costs show up, people feel like they failed at budgeting.

The truth is that irregular expenses are normal. Sinking funds categories help you plan for them in advance. They reduce financial stress, limit the need for credit cards, and help you stay consistent with your money goals. They also make your budget feel more honest because it reflects the full picture of your financial responsibilities.

Best Sinking Funds Categories to Include in Your Budget

Not every person needs the same categories, but some sinking funds are useful for almost everyone. The goal is to create categories based on your lifestyle, family needs, and financial priorities.

1. Car Maintenance and Repairs

Car expenses are one of the most common reasons people go over budget. Oil changes, tire replacements, brake work, and unexpected repairs can be expensive. A car sinking fund helps you prepare for both routine maintenance and surprise fixes.

Even if your vehicle is currently in good condition, setting aside a small amount each month can save you from panic later.

2. Home Maintenance

If you own a home, repairs and maintenance are unavoidable. You may need money for plumbing, paint, appliances, yard care, or seasonal upkeep. A home sinking fund can help cover these costs without relying on credit.

Even renters may want a small household fund for furniture, cleaning supplies, or replacement items.

3. Holiday and Christmas Expenses

Holiday spending can quickly get out of control when you do not plan for it. Gifts, decorations, travel, food, and events can add up fast. A dedicated holiday sinking fund allows you to enjoy the season without damaging your finances.

This is one of the most popular sinking funds categories because it turns a stressful season into a manageable one.

4. Birthdays and Celebrations

Birthdays, anniversaries, weddings, baby showers, and graduation gifts often catch people off guard. But these events happen regularly, so they should have a place in your budget. Saving gradually throughout the year makes it easier to celebrate loved ones without financial pressure.

5. Medical and Health Expenses

Even with insurance, health costs can still appear unexpectedly. Co-pays, prescriptions, dental work, glasses, and specialist visits can all put pressure on your monthly budget. A medical sinking fund creates a cushion for those expenses.

This category is especially helpful for families, people with ongoing health needs, or anyone with a high-deductible plan.

6. Back-to-School Costs

If you have children, school expenses are rarely limited to one shopping trip. Supplies, uniforms, activity fees, books, lunches, and special events can all require extra money. A back-to-school sinking fund helps spread out those costs over time.

7. Vacation and Travel

Travel is much more enjoyable when it is fully funded in advance. A vacation sinking fund can cover transportation, hotels, food, entertainment, and spending money. Even a short weekend trip becomes less stressful when the money is already waiting.

8. Annual Bills and Subscriptions

Some bills only come once or twice a year, but they are still important. These may include insurance premiums, memberships, professional fees, taxes, or software renewals. Since the due dates are known, these are perfect expenses for sinking funds.

This is one of the smartest sinking funds categories because it prevents those large yearly payments from catching you off guard.

How to Choose the Right Sinking Funds Categories

The best way to choose your categories is to review your past spending. Look at the expenses that tend to show up every few months or once a year. Ask yourself which costs usually feel stressful or force you to dip into savings.

You do not need a long list at first. Start with three to five categories that matter most. Focus on the expenses that happen often or cost the most. Over time, you can add more categories as your budgeting system becomes stronger.

Keep your list practical. Your sinking funds should support your real life, not make your budget more complicated than necessary.

Tips for Managing Sinking Funds Successfully

To make sinking funds work, consistency matters more than perfection. Decide how much you need for each category and divide that amount by the number of months until you need it. Then contribute that amount regularly.

You can keep your sinking funds in separate savings accounts, budgeting apps, envelopes, or simple tracking spreadsheets. The method does not matter as much as staying organized and committed.

It is also helpful to review your categories every few months. Your needs may change, and your budget should change with them.

Final Thoughts on Sinking Funds Categories

Using sinking funds categories is one of the easiest ways to make your budget more realistic and less stressful. Instead of being surprised by predictable expenses, you prepare for them one step at a time. That creates peace of mind, reduces debt, and gives you greater control over your money.

Whether you start with holiday savings, car repairs, medical bills, or annual subscriptions, the important thing is to begin. Small monthly contributions can lead to major financial relief. Once you start using sinking funds, you may wonder how you ever budgeted without them.